The Population Paradox

Eastern Europe has been losing people for decades. It has also been getting richer. Does that make the demographic doomers wrong—or merely premature in their predictions?

On the banks of the Danube in Bulgaria’s remote northwest, where the country meets Serbia and Romania, lies the city of Vidin, a place that one could, if in a generous mood that day, call pleasantly sleepy.

Walking through Vidin today, it is sometimes hard to tell where the city ends and the forest begins. Vines curl around concrete balconies; linden trees line streets that each year see fewer pedestrians. If one were to use a more boorish term, the city might also be just dying.

At least, that’s what some of its natives believe, such as Ognyan. He described what it felt like to return after having worked elsewhere: “It was as if I were coming back to my grave. This is a dying city.”

The population of Vidin declined from 62,690 in 1992 to only 38,669 in 2022, an almost 40% decline. The city is the center of the eponymous region, where the situation is even more dire. It has less than half the population it had in 1992, and it has been declining due to urbanisation since 1946, when its population peaked at almost 200,000 people.

Fewer Bulgarians, Richer Bulgaria

The region is among the poorest and worst-performing in Bulgaria, and in the whole of the European Union: GDP per capita in purchasing power parity reaches only about a third of the EU average, median life expectancy stands at around 73 years, and the number of people retiring each year is roughly double the number of those entering the workforce.

Bulgaria as a whole is faring only a little better. The population of the country declined from almost 9 million in 1985 to 6.4 million today, driven by both natural decline and emigration to wealthier parts of Europe. Bulgaria thus holds—or at least held for decades, until the war in Ukraine possibly handed that title to Ukraine—the unflattering distinction of being the country with the largest population loss in the world.

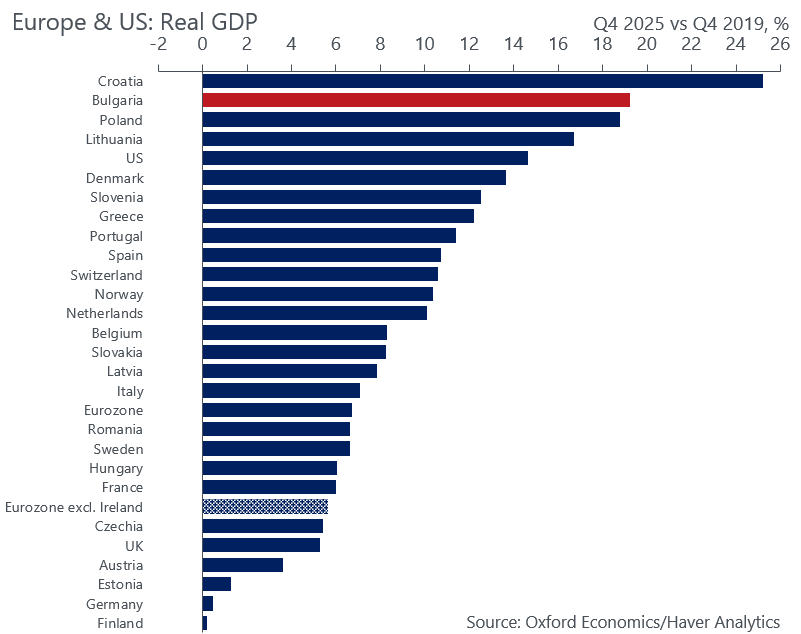

And yet Bulgaria has not been doing badly economically. While it remains the poorest EU country, it rose from 40% (in 2007, when it entered the EU) of the EU average for GDP at purchasing power parity per capita to 68% in 2025.

Its GDP growth in the past couple of years has been among the highest in the EU, with output one fifth larger than pre-pandemic figures, second only to Croatia and ahead of both Poland and the United States. Recently it has experienced a massive surge in industrial investment, especially in machinery. Even as its population declines and ages—the median age increased from 35 to 47 between 1989 and 2024—it does not seem to be slowing its economic growth all that much.

Bulgaria is not the only example of this trend by any means—post-communist Europe is rather full of them. Lithuania and Latvia have lost 20% of their population between 2000 and 2019, and their median age increased from the early thirties in 1989 to 44 in 2024.

Yet the GDP per capita of Latvia and Lithuania increased by 140% and 168% respectively over that same period. Demographic decline and its economic fallout are very often portrayed in a highly doom-inducing manner—the last few young workers in the year 2064 will be crushed to death by the falling pieces of a collapsing pension system, or so this sort of prediction goes.

Yet for many countries, population ageing and decline is increasingly not something which belongs to a distant and abstract future; it is the reality on the ground, in the here and now.

There is quite an abundant body of scientific literature dealing with precisely this question: is the demographic decline we are entering into truly an economic catastrophe in the making, or does the doomerist narrative really point to a cultural anxiety about peoples vanishing, but which is dressed up as an economic issue—since that is the language the contemporary homo economicus tends to understand best? Let’s find out.

A Matter of Measurement

The economy can be measured in two fundamental ways: as its aggregate size—overall GDP—and in per capita terms. The former is better suited to assessing the economic weight of a country in international relations and geopolitical competition; great powers simply must have large populations. In terms of overall GDP growth, population growth of course matters a great deal—alongside capital, labour is one of the basic factors of production. Nevertheless, when it comes to the living standards of ordinary citizens, per capita measurement is what one needs to look at. Here, the picture changes considerably.

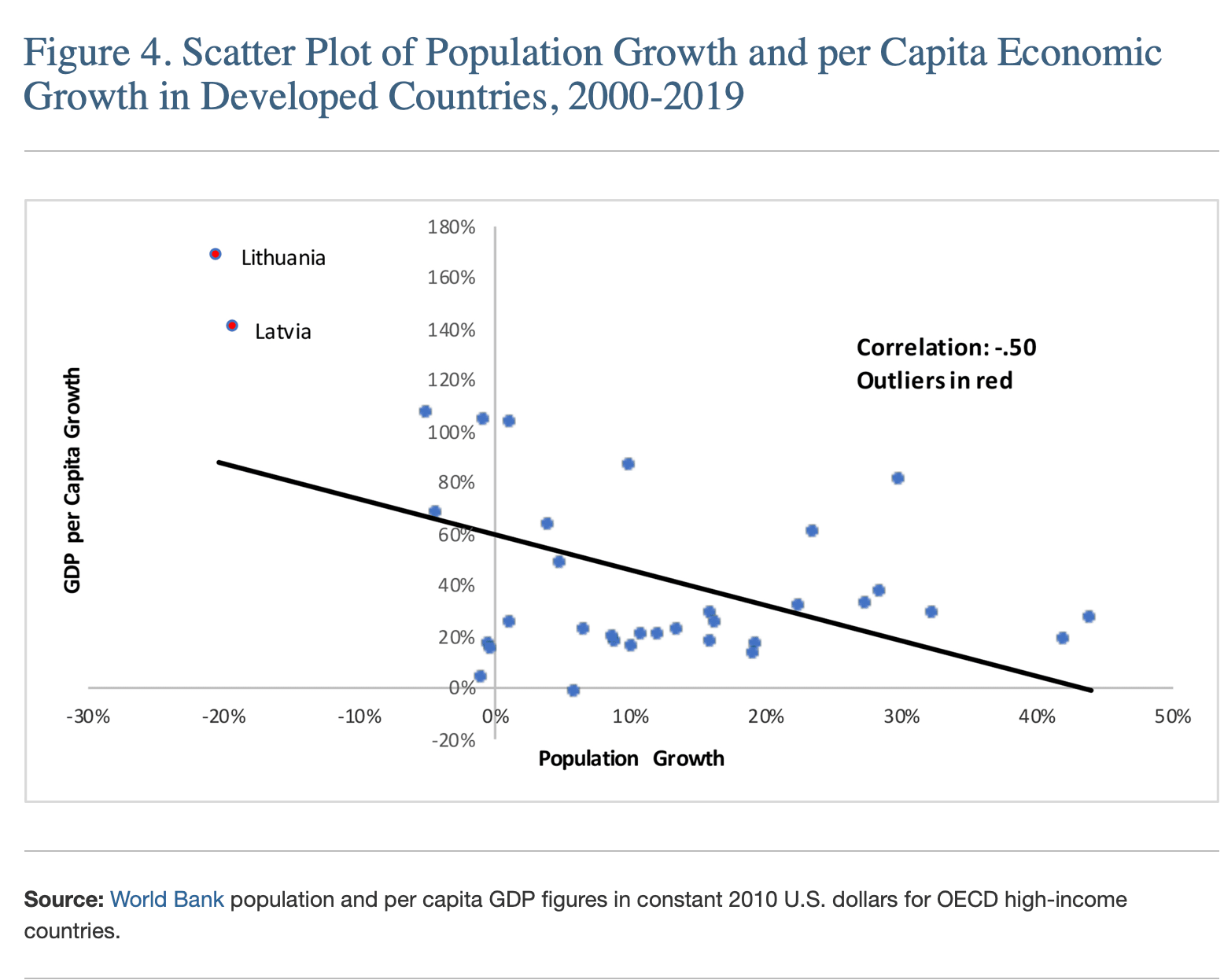

A study by the Center for Immigration Studies found that among high-income OECD countries, the correlation between population growth and per capita GDP growth over the 2000–2019 period was negative at −0.50—a relatively strong relationship.

Countries losing population grew more in per capita terms than those gaining it. It is worth noting that CIS is a think tank advocating for restrictive immigration policy in the United States, so a degree of bias cannot be excluded. The negative correlation may also be partly mechanical: when you divide by a shrinking population, per capita GDP rises faster almost by definition.

There are further reasons to treat this correlation with caution. Roughly two thirds of the states in the sample with declining populations are post-communist countries in Eastern Europe. One could argue that communism was a system of such profound economic retardation that countries adopting capitalism will tend to grow rapidly almost regardless of circumstances—unless the transition is thoroughly botched.

This interpretation is supported by the fact that post-communist countries tend to be consistent underperformers in correlations between national IQ and wealth: they are considerably poorer than their human capital metrics would predict, suggesting an institutional deficit left by the communist era that capitalism has been steadily undoing. The data further show that the poorest post-communist countries grew the fastest, lending additional support to the hypothesis that it is more about technological and institutional convergence allowing growth despite population decline.

Moreover, the study’s choice of 2000 as its starting point introduces a certain bias of its own, since many post-communist economies endured extremely turbulent conditions throughout the 1990s; had the window begun in 1990, the correlation would likely be considerably weaker. Yet the pattern is not confined to post-communist transition economies. Japan, Italy, and Portugal—countries with very different institutional histories and no communist legacy to undo—show the same result: population declining, GDP growing. If the effect was purely an artefact of a post-communist catch-up, we would not expect to find it there.

There is also the crucial question of human capital: immigrants account for the majority of population growth in almost all developed countries, yet different immigration sources produce very different economic outcomes—the studies measure population growth in purely quantitative terms, collapsing what is in reality an enormously heterogeneous phenomenon into a single number. This points to a deeper issue with the demographic framing altogether. What drives long-run economic growth is not necessarily the quantity of people but the stock of knowledge and skills they carry—and that stock can grow even as the population shrinks, provided each smaller generation is better educated or more intelligent than the last.

Two Questions, Two Answers

As another study shows, the debate on demographics tends to conflate two questions that might have very different answers: what is good for government budgets, and what is good for people’s actual living standards.

On public finances, the pessimists have a point. Pension and healthcare systems were built on the assumption that each generation of retirees would be backed by a larger generation of taxpayers. When fertility falls, that assumption gives way as the fiscal arithmetic becomes unworkable.

The same logic applies to government debt: states carrying large debt-to-GDP ratios are under strong pressure to grow their headline GDP figures by any means necessary to avoid fiscal crisis, and frequently turn to large-scale immigration as the most readily available lever to pull.

But living standards follow a different logic. Smaller families tend to invest more in each child, producing a smaller but more productive next generation. A tighter labour market pushes wages up. And when an already shrinking cohort of workers becomes scarce, firms face stronger incentives to automate the tasks those workers perform.

This is not merely theoretical: Japan, Germany and South Korea, which are ageing faster than the United States, all have significantly higher robot density in manufacturing, and research estimates that demographic change alone explains between 40 and 65 percent of cross-country variation in industrial robot adoption. The net effect is that moderately low fertility—roughly 1.5 to 2.0 births per woman—tends to maximise consumption per capita rather than undermine it.

Nevertheless, below 1.5 the calculus shifts. Demographic contraction begins to outpace the gains from higher human capital investment, dependency ratios deteriorate sharply, and the intergenerational transfers that hold welfare states together come under genuine strain. The problem is that the number of countries managing to keep fertility within the 1.5–2.0 range continues to shrink. And while the tension between the fiscal interests of the state and the material wellbeing of its citizens is analytically interesting, it has its limits as a distinction. If the state comes under acute fiscal stress, its population will pay the price one way or another—usually through reduced benefits, higher taxes, or both.

The Bill Is Still Due

Yet it is important not to get overly optimistic. Most of the studies we have looked at so far are retrospective—they examined how countries have been faring up to now. Future headwinds will be of a different magnitude. In Bulgaria, the number of retirees per 100 workers stands at 35 today. In Japan, the oldest country on earth, it is over 50. A few decades from now, few countries will have figures better than Japan does today; Bulgaria is projected to reach around 60.

According to a McKinsey report from 2025, GDP per capita growth in heavily affected countries could slow by an average of 0.4 to 0.8 percentage points annually through 2050—unless productivity rises at two to four times its current rate. Looking at the average per capita growth of high-income countries, it becomes clear that for many of them—France, Canada, Italy, Spain—a reduction of that magnitude would mean essentially zero or negative per capita growth. Meanwhile, pension systems may need to absorb as much as half of all labour income simply to bridge the widening gap between what retirees consume and what they earn.

What would a labour productivity growth of two to four times actually look like? One of the few countries that has more than doubled its productivity since 2000 is South Korea—a technological powerhouse that directs around 5% of GDP toward research and development. Other strong performers with comparable or better capabilities include the best-performing post-communist states, such as Poland and Lithuania. Yet here one notices an uncomfortable statistic connecting these countries. South Korea’s fertility rate has fallen below one child per woman; Poland’s and Lithuania’s sit barely above one. This may be no coincidence: low fertility frees up women for the workforce, concentrates household investment into fewer children, and compresses consumer spending into a smaller but more productive population—all of which can turbocharge growth in the short and medium term.

But it also means that the exceptional productivity growth these countries achieved was in part made possible by the very demographic decline that now demands they sustain it indefinitely. The growth was real, but some of it was borrowed from the future. The bill is still due.

And for many wealthy Western nations, this kind of growth—catching up with the technological innovations in the case of Poland and Lithuania, or East Asian-style workaholism in the case of South Korea—is simply not a realistic template to follow. Maybe artificial intelligence will unlock productivity gains previously unimaginable and resolve all of this—yet if something sounds too good to be true, it usually is.

Set aside the technological deus ex machina, and the picture that emerges is quite paradoxical. Many Western countries, such as the United States, Australia, the United Kingdom, France, and Sweden, had decades of experience with mass immigration while managing to keep fertility rates within the 1.5–2.0 Goldilocks zone identified by researchers. That influx was more often than not justified by the alleged needs of an economy short of workers.

As the data suggests, that justification was probably false, and per capita growth in these countries might well have been stronger without it. Japan’s per capita growth over the past two decades exceeded that of a number of these countries—including France, the United Kingdom, Australia and New Zealand—despite highly restrictive immigration and a deliberate pivot toward automation.

Yet it is also true that in the coming decades, as the fertility rate in more and more countries plunges to levels previously unseen and its effects compound over time, labour shortages and fiscal pressure on welfare systems will become very real. Many political establishments may find that they have completely exhausted whatever trust they had by pushing mass immigration in times when it was barely necessary, leaving their societies polarised and fractured precisely at the moment when managed, well-considered immigration would have been genuinely useful.

Cities like Vidin—pleasantly sleepy, or dying, depending on one’s interpretation—will nevertheless be an inevitable part of the world we are building.

| A guest post by

|

It is quite obvious that South Korea and Poland greatly capitalised on their demographic dividend. Their major growth period corresponds with the window of time after fertility fell but strong cohorts were not yet entering retirement age. Dependency ratios went down, the economy was awash in high human capital workers. (If Poland wasn't suffering from the aftershocks of communism and didn't lose so many people to emigration because the economy was unable to fully utilise them, it would have been much richer and stronger today).

But the chickens are coming home to roost now.

Something to add that wasn't mentioned in the article is that once population starts shrinking capital per worker goes up. Japanese having a higher productivity per worker makes sense as there is more money, tools, resources available. A nuclear plant or a car factory will still be usable even 50 years from now, but the working population might be just a fraction of what it was when those things were built.